This article is featured in Bitcoin Magazine “The question of registrations”. Click on here to get your annual subscription to Bitcoin Magazine.

Click here to download a PDF of this article.

Ordinals have been a polarizing phenomenon for most Bitcoin subcommunities, with the exception of miners.

The meteoric rise of Bitcoin's new native NFT standard dominated the discourse for months as ordinals flooded the block space and propelled transaction fees to multi-year highs. Critics say these transactions are, at worst, an attack on Bitcoin that has tainted the sanctity of a scarce block space; at best, they are shitcoins, the playthings of players that belong to casino chains like Ethereum.

Well, miners don't care if they are shitcoins. They don't care about making money, and Ordinals gave them a revenue boost at a time when mining revenues were at one of their lowest levels ever. Many miners adopted – or at least are ambivalent about – ordinals/registers because they received a much-needed boost to Bitcoin mining profitability when many miners were near breakeven or unprofitable.

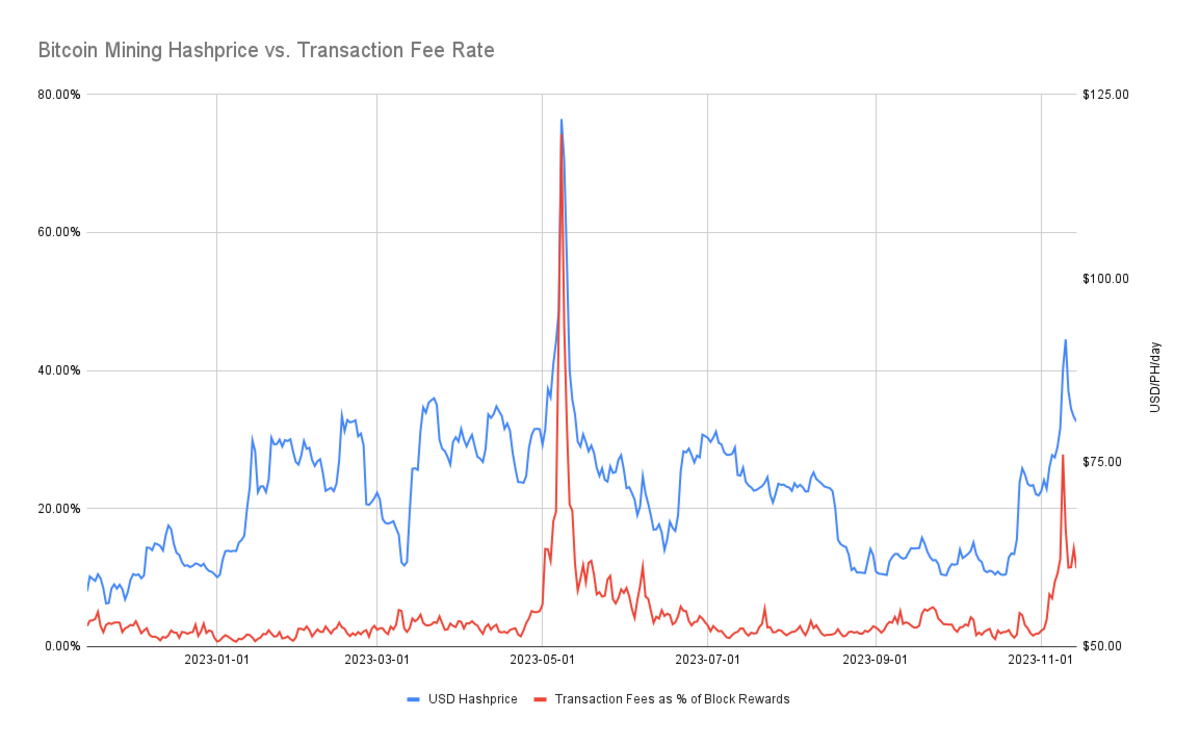

Hash price is a measure of how much USD (or BTC) miners can expect to earn from a unit of hashrate (e.g. at $80/PH/day, a miner with 1 petahash of rigs mining – around 10 new generation ASICs like the S19j Pro, for example, can earn $80 per day).

Given their positive impact on the hashprice, Ordinals, a technical breakthrough that few could have predicted last year, have found themselves at the center of discussions regarding the mining economics of Bitcoin, discussions more relevant with each block which brings us closer to the fourth block of Bitcoin. subsidy cut in half.

I'm not writing this to encourage anyone to become an Ordinals fan. Personally, I don't really understand the appeal. But I think they are important in the context of Bitcoin's ever-decreasing overall subsidies, so they are worth studying to understand how they affect the block space and mining economics – and what such developments could mean in a future where only minors exist. on transaction fees.

WTF is an ordinal, anyway?

In NFT parlance, people use Ordinal and Inscription interchangeably, but the individual terms refer to two different aspects of the NFT standard.

An inscription is a work of art or digital media, while an ordinal is technically the number prescribed to an inscription to mark its place in the grand scheme of all other inscriptions. Another way to look at it is that the inscription itself is the NFT, while the ordinal is the number used to identify an individual inscription.

The data for each registration can be found in the separate witness section of a transaction. As such, unlike other NFT standards, art, digital media or data is uploaded directly to the Bitcoin blockchain. Since the listings are entirely on-chain, one could argue that these are the purest form of NFT available as they benefit from the immutability of the blockchain.

Not all listings are equal

When you understand that signups are real on-chain data, you can appreciate some of the criticisms and concerns of detractors; if a bunch of NFT degens are listing monkey JPEGs, dickbutts, and God knows what else on the chain, then that crowds out economical (and potentially necessary) transactions.

This concern has been compounded by the fact that each listing's arbitrary data receives a transaction fee discount. As a scalability measure, Bitcoin's segregated witness upgrade changed the transaction structure so that witness data for a private key signature and a public key were moved from the hash field of the transaction to another part of the block. Bitcoin shrinks SegWit data, so it requires fewer satoshis per byte in transaction fees to complete a transaction. Arbitrary data for a registration is in the SegWit field of a transaction, so it is entitled to the SegWit discount. Wave to the pitchforks.

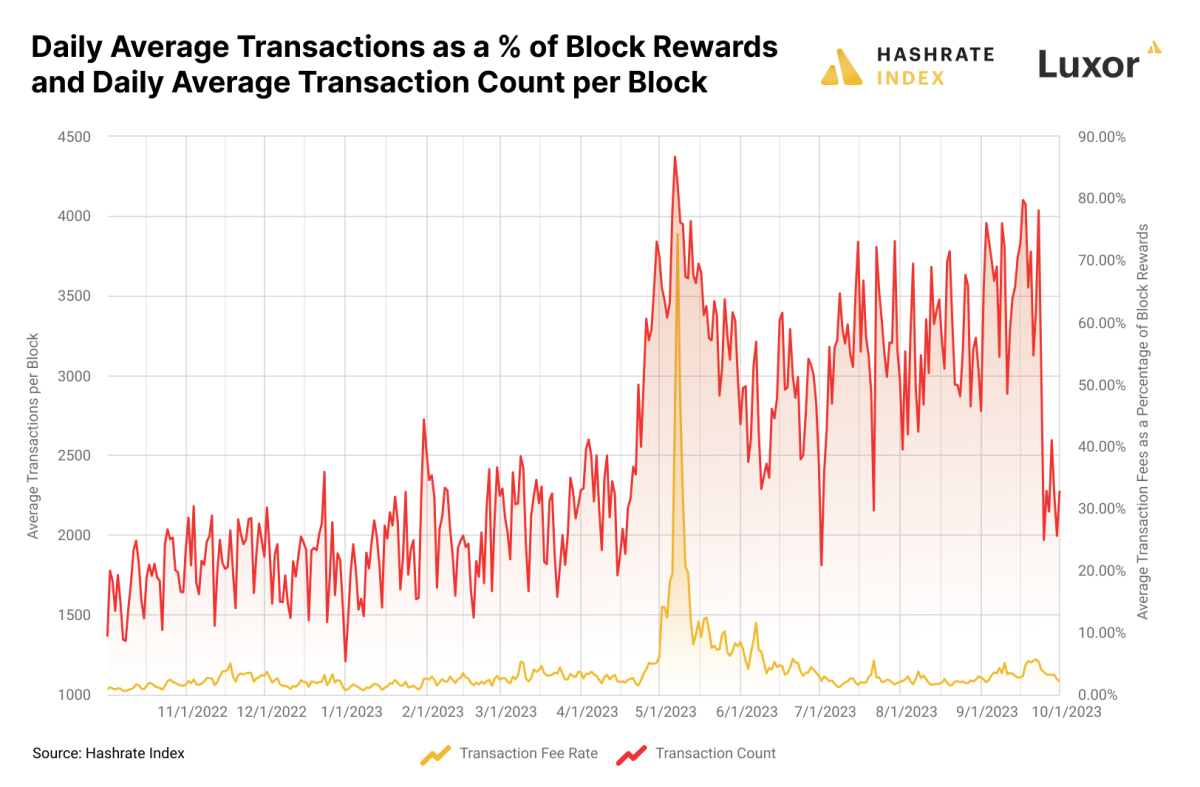

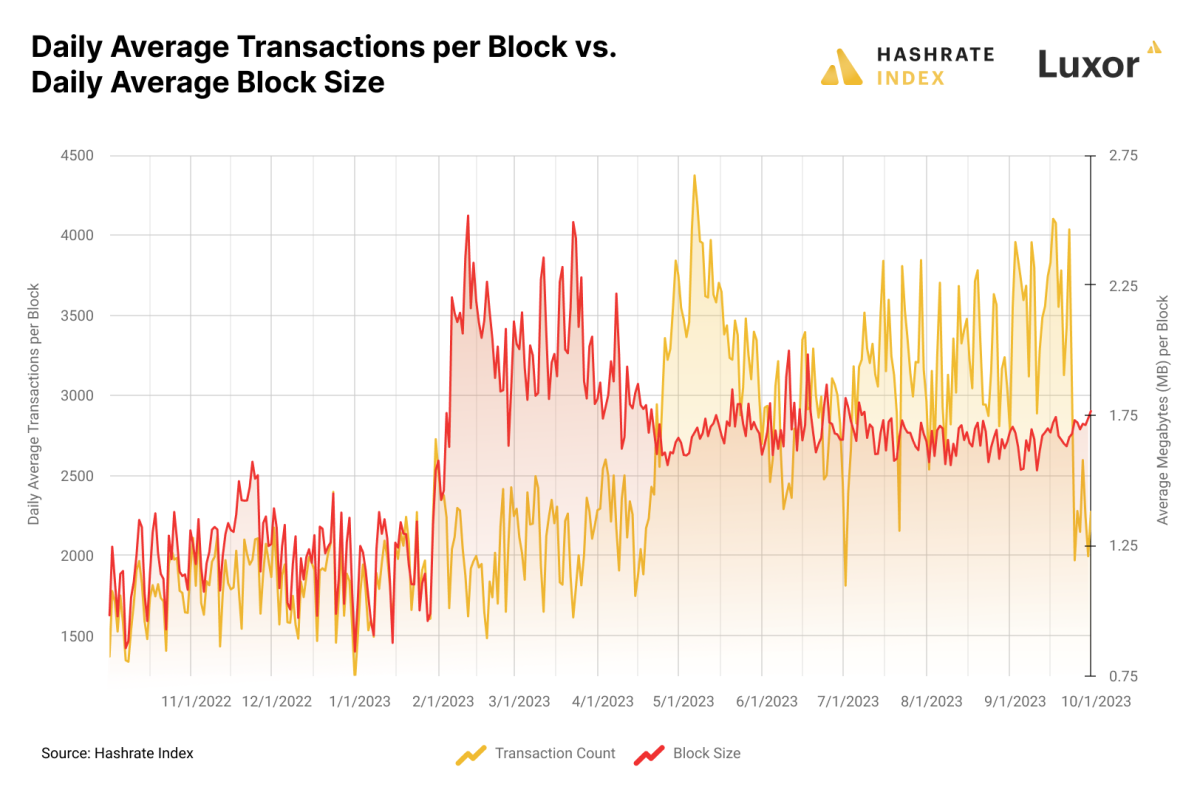

This discount is why, despite the first wave of image-based registrations crowding block space in February/March/April, transaction fees have not increased significantly; block sizes increased as forward-thinking enrollers dumped the blockchain with thousands of JPEG files for early listing collections, but these all benefited from SegWit's 4-to-1 data reduction compared to normal transactions. Perhaps intuitively, it was only when the less data-intensive text listings of BRC-20 tokens became the most popular type of listing that transaction fees skyrocketed.

The so-called BRC-20s (a nod to Ethereum's ERC-20 token standard) are a free form of token. I say loose because they are really just ordinals in a series defined by Bitcoin's OP_CODE function, where each “token” is itself an OP_CODE transaction which defines the token's place in the BRC series -20 specific. It happens like this: someone (God only knows who) posts an OP_CODE transaction which sets the token series' maximum supply, ticker, and minting limit per transaction. Once made public, anyone with the technical know-how can create tokens in the series.

These OP_CODE transactions don't benefit from SegWit's data discount, so they cost a pretty penny more than image-based signups. But they also have a feature that image listings don't have: the minting feature, which brings Ethereum NFT-like incentives to collecting these listings. Ethereum NFT series typically have minting contracts where anyone can mint new NFTs in the series by interacting with the contract. That’s part – if not all – of the appeal. Creating an NFT is like opening a digital pack of Pokémon/baseball/Magic: The Gathering cards – there might be a rare card in the next one!

And while there isn't necessarily the possibility of creating a rare BRC-20 (since they're all the same), there is the possibility of creating a bunch of NFTs in a hot new series. Why anyone cares about having ORDI/CUMY/RATS #1 or #100 or whatever, I don't know. This is perhaps the greatest expression of the Biggest Fool Theory yet in Bitcoin. But the fact is that it is, and the incentives to mint BRC-20s have precipitated the largest wave of Bitcoin transaction activity ever seen.

Thanks to a combination of fee wars and the fact that these NFTs don't benefit from the SegWit discount, the BRC-20s have put on a veritable fee feast for Bitcoin miners, but not exactly in the way you might think.

Quantifying collateral damage linked to transaction fees

The majority of transaction fee increases in 2023 do not come directly from fees associated with ordinals; this comes from indirect fee pressure on other transactions.

According to data from independent analyst Data Always' Dune dashboard, as of November 12, 2023, miners have raked in $70.3 million in fees from Ordinals. That sounds huge, but it only represents 19.4% of the $368.2 million in transaction fees that miners have earned in total since registrations began on December 14, 2022. To put that into perspective, there is had 40.2 million registration transactions, which equates to 30%. of total trading volume since December 14. So registrations accounted for a third of trading volume over the past year, but only a fifth of all fees.

As for other fees, many of them are the result of indirect pressure from registration fees – that is, fees that do not come directly from the registrations themselves, but from the pressure that the registrations exercise on the average transaction fees needed to clear a Bitcoin transaction. within a reasonable time.

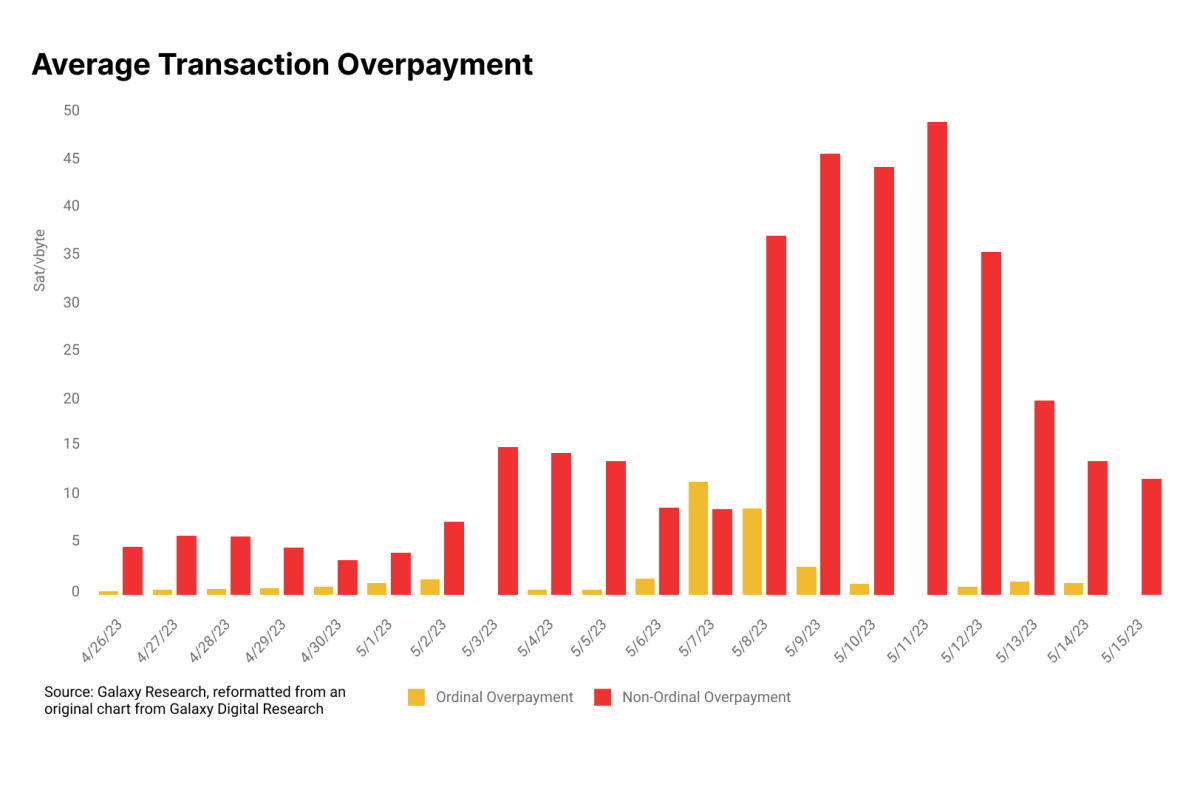

Galaxy Digital Research examines this dynamic in a report titled “Bitcoin Inscriptions & Ordinals: A Maturing Ecosystem.” Rampant write activity is cluttering the memory pool. This is especially true during BRC-20 minting events, as first come, first struck encourages bidding wars as registrants attempt to be the first to mint a series. This raises the floor for average transaction fees and, as Galaxy Digital Research points out, precipitates “overpayment” of transaction fees from various operators. They define overpayment as any fee in a block that is greater than the median transaction fee of that block. For normal transactions, this overpayment could arise from transaction fee estimators in wallets or on exchanges or from users' general ignorance regarding the structure and dynamics of transaction fees. Some users may also have to speed up their transactions for various reasons, thereby resulting in an overpayment. For registration transactions, Galaxy Digital Research claims that “willful overpayments” were common during periods of high activity and popular registration workshops.

This chart quantifies overpayments for registration transactions and all other transactions to demonstrate the dynamics described by Galaxy Digital Research in its report. When Bitcoin's memory pool lagged in April and May – the hottest period for listing activity so far – the majority of transaction fees during that period actually came from too much. paid from users for financial transactions, not from the registrations themselves. These users could probably make things easier for themselves by not using built-in transaction fee estimators with their wallets and exchanges.

Blessing and curse

Listings are a blessing and a curse. They are a boon for miners, but they can be very painful for other Bitcoiners, especially those who have to send transactions across the network on a daily basis.

That said, blockspace is an open market. So I don't have to like the Ordinals to recognize that it's not my place to control someone else's spending. It's also not my place to censor a transaction that pays for block space on the open market. After all, that's part of the point of a permissionless blockchain: to make transactions that other people don't want you to do.

This article is featured in Bitcoin Magazine “The question of registrations”. Click on here to get your annual subscription to Bitcoin Magazine.

Click here to download a PDF of this article.