Introduction

Founded in 1989, MicroStrategy is an American company that provides business intelligence, mobile software and cloud-based services. Led by Michael Saylor, one of its three co-founders, the company had its first major success in 1992 after landing a $10 million contract with McDonald’s.

Throughout the 1990s, MicroStrategy saw its revenue increase by more than 100% per year by positioning itself as a leader in data analysis software. The onset of the dot.com boom in the late 1990s spurred the company’s growth and peaked in 1998 when it went public.

And while the company has been a staple of the global trading environment for decades, it wasn’t until it acquired its first Bitcoins in August 2020 that it slipped under the crypto industry’s radar.

Saylor made news by making MicroStrategy one of the few public companies to hold BTC as part of its cash reserve policy. At the time, MicroStrategy said its $250 million investment in BTC would provide a reasonable hedge against inflation and allow it to earn a high return in the future.

Since August 2020, the company has been periodically buying large amounts of Bitcoin, affecting both the price of its stock and BTC.

At the time of MicroStrategy’s first Bitcoin purchase, BTC was trading at around $11,700, while MSTR was trading at around $144. At press time, the price of Bitcoin is hovering around $22,300 while MSTR closed the previous trading day at $252.5.

This represents a decrease of 75.6% from MSTR’s July 2021 high of $1,304. Combined with Bitcoin’s price volatility, the company’s steep stock price decline over the past two years has caused many to criticize MicroStrategy’s cash management strategy and even actively sell it.

In this report, CryptoSlate dives deep into MicroStrategy and its holdings to determine whether its ambitious Bitcoin bet is making its stock currently undervalued.

MicroStrategy Bitcoin Holdings

Since March 1, 2023, MicroStrategy held 132,500 BTC acquired at a total purchase price of $3.992 billion and an average purchase price of approximately $30,137 per BTC. Bitcoin’s current market price of $22,300 puts MicroStrategy’s BTC holdings at $2.954 billion.

The company’s Bitcoins were acquired through 25 different purchases, with the largest being made on February 24, 2021. At the time, the company purchased 19,452 BTC for $1.206 billion while BTC was trading just under of $45,000. The second largest purchase was made on December 21, 2020, when he acquired 29,646 BTC for $650 million.

At Bitcoin’s ATH in early November 2021, the 114,042 BTC MicroStrategy held were worth well over $7.86 billion. Bitcoin’s plunge to $15,500 in early November 2022 valued the company’s holdings at just over $2.05 billion. At the time, the market capitalization of all MSTR shares reached $1.90 billion.

As CryptoSlate’s analysis showed, it wasn’t until late February 2023 that MicroStrategy’s market capitalization became equal to the market value of its Bitcoin holdings. The discrepancy between the two is what has many wondering if MSTR might be undervalued.

However, to determine overvaluation or undervaluation, it is not enough to look at MicroStrategy’s market capitalization.

MicroStrategy’s debt

The company issued $2.4 billion in debt to fund its Bitcoin purchases. As of December 31, 2022, MicroStrategy’s debt consists of the following:

- $650 million 0.750% convertible senior notes due 2025

- $1.05 billion 0% convertible senior notes due 2027

- $500 million 6.125% senior secured notes due 2028

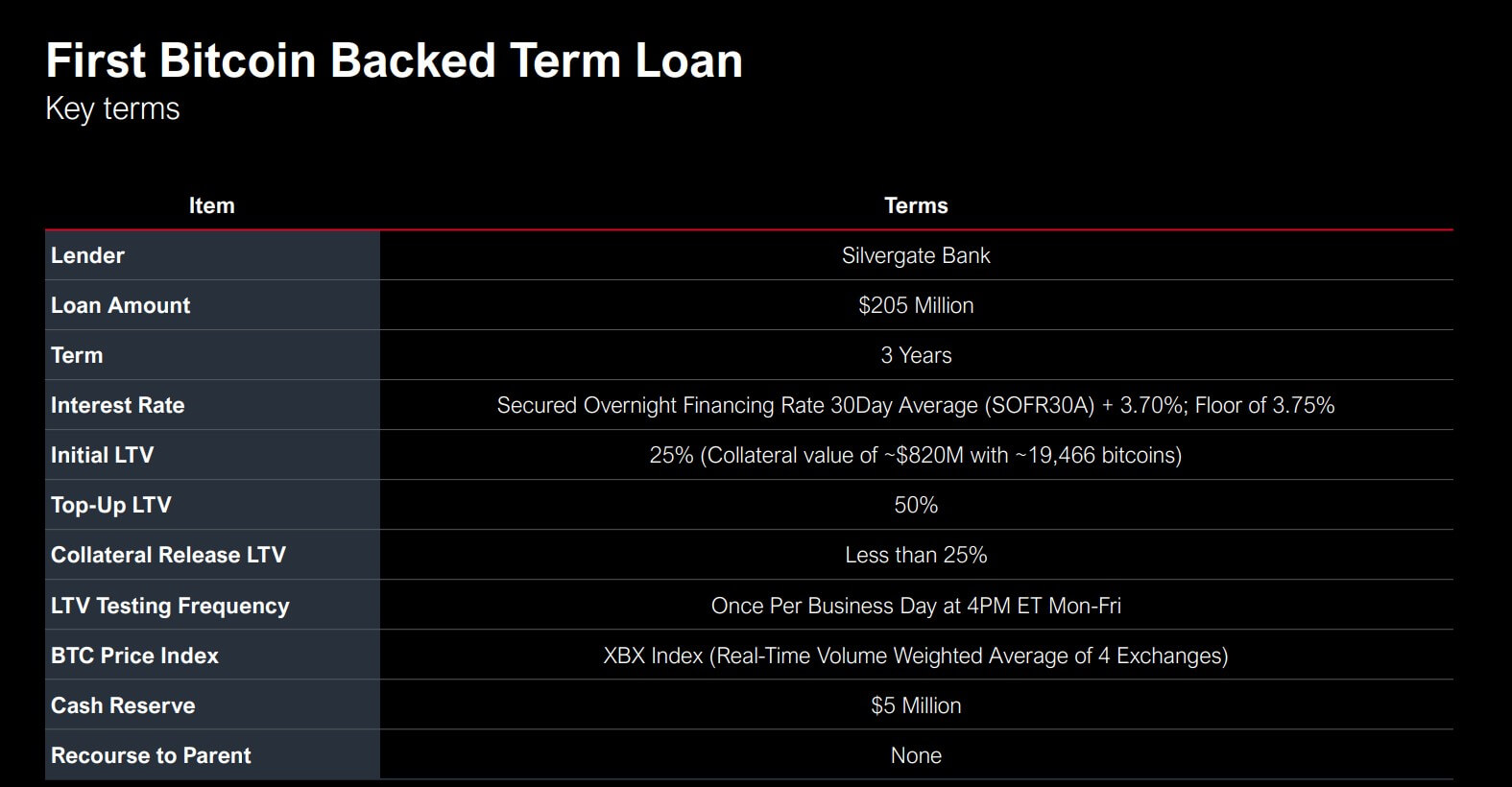

- $205 million under a secured term loan

- $10.9 million of other long-term debt

The rates the company has earned on the 2025 and 2027 convertible bonds have proven extremely beneficial, especially in light of the recent rise in interest rates. However, the benefits MicroStrategy accrued on the convertible notes are outweighed by the risks it took with its $205 secured term loan from Silvergate Bank in March 2022.

The loan was secured by 19,466 BTC, worth $820 million at the time, with an LTV ratio of 25%. Until its maturity in March 2025, the loan must remain secured with a maximum LTV ratio of 50% – if the LTV exceeds 50%, the company will have to top up its collateral to bring the ratio down to 25% or less.

The Terra crash in June 2022 caused volatility in the market that forced MicroStrategy to deposit an additional 10,585 BTC in collateral. In addition to volatile Bitcoin prices, Silvergate’s floating rate loan resulted in an annualized interest rate of 7.19%, which put significant pressure on the company.

The recent Silvergate controversy, covered by CryptoSlate, has many people worried about MicroStrategy’s lending future. However, the company noted that the future of the loan does not depend on Silvergate and that the company continue repay the loan even if the bank goes bankrupt.

Of the 132,500 BTC the company holds, only 87,559 BTC are unencumbered. In addition to the 30,051 BTC used as collateral for the Silvergate Secured Term Loan, MicroStrategy has posted 14,890 BTC as collateral for the 2028 senior secured notes. If the Silvergate loan collateral were to be completed, the company could tap into the unencumbered 87,559 BTC.

Saylor also noted that the company could post further collateral if Bitcoin’s price falls below the $3,530 that would trigger a margin call on the loan.

MSTR vs. BTC

One of the biggest stars of the dot com boom, MicroStrategy has seen its stock go through periods of intense volatility in times of expansion.

Following its IPO in 1998, MSTR saw its price increase by over 1,500%, peaking in February 2000 at over $1,300. After a dramatic price crash that marked the start of the dot com crash, it took the company more than a decade to regain the $120 stock price it was at in 1998.

Prior to its first Bitcoin purchase in August 2020, MicroStrategy’s stock was trading at $160. September caused a notable rally that pushed its price to a new high of $1,300 in February 2021.

Since then, MSTR has shown a notable correlation with Bitcoin price movements, with the company’s performance now tied to the crypto market.

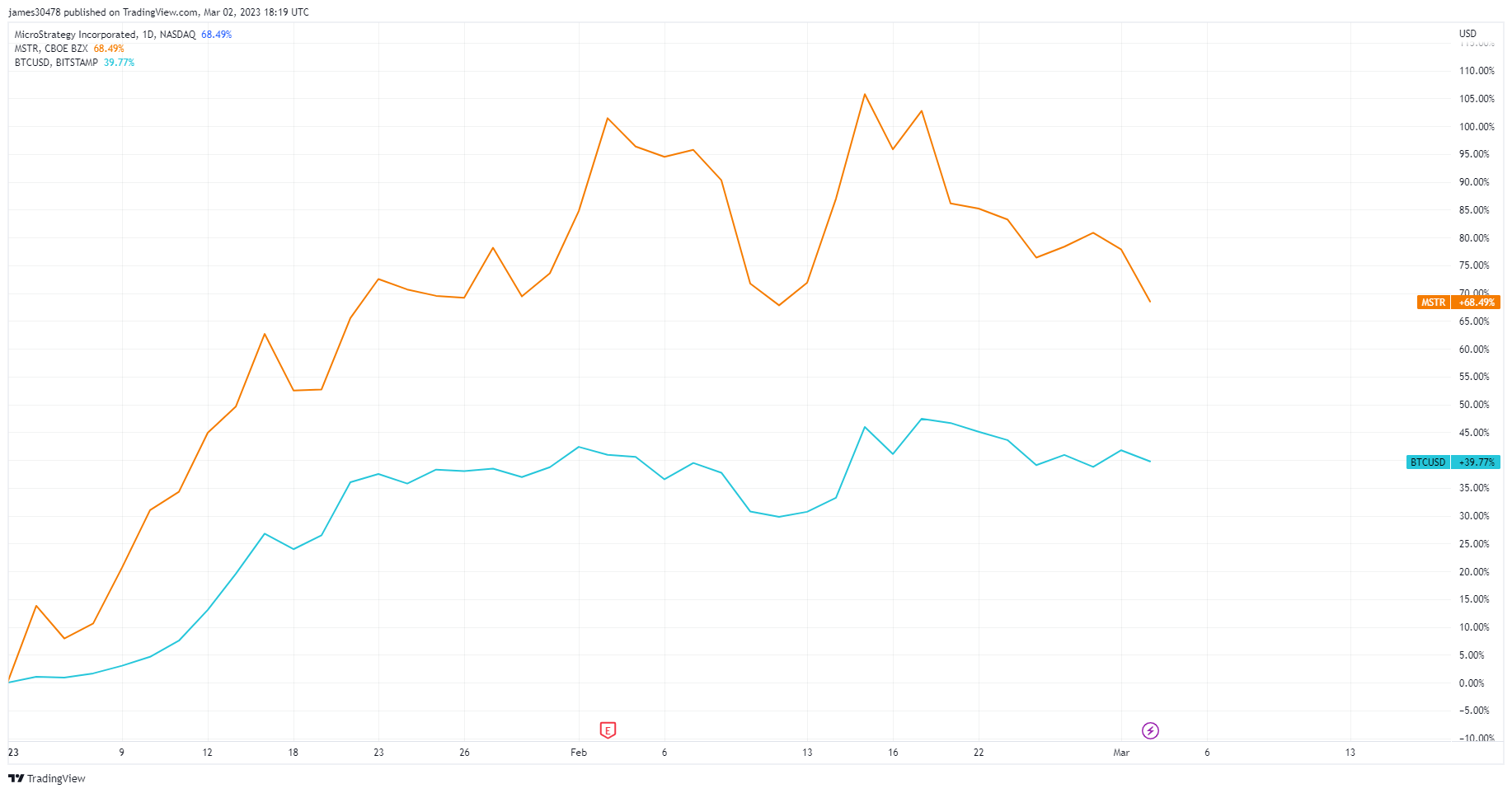

Up over 68% year-to-date, MSTR has outperformed BTC, which has seen its price rise just under 40%.

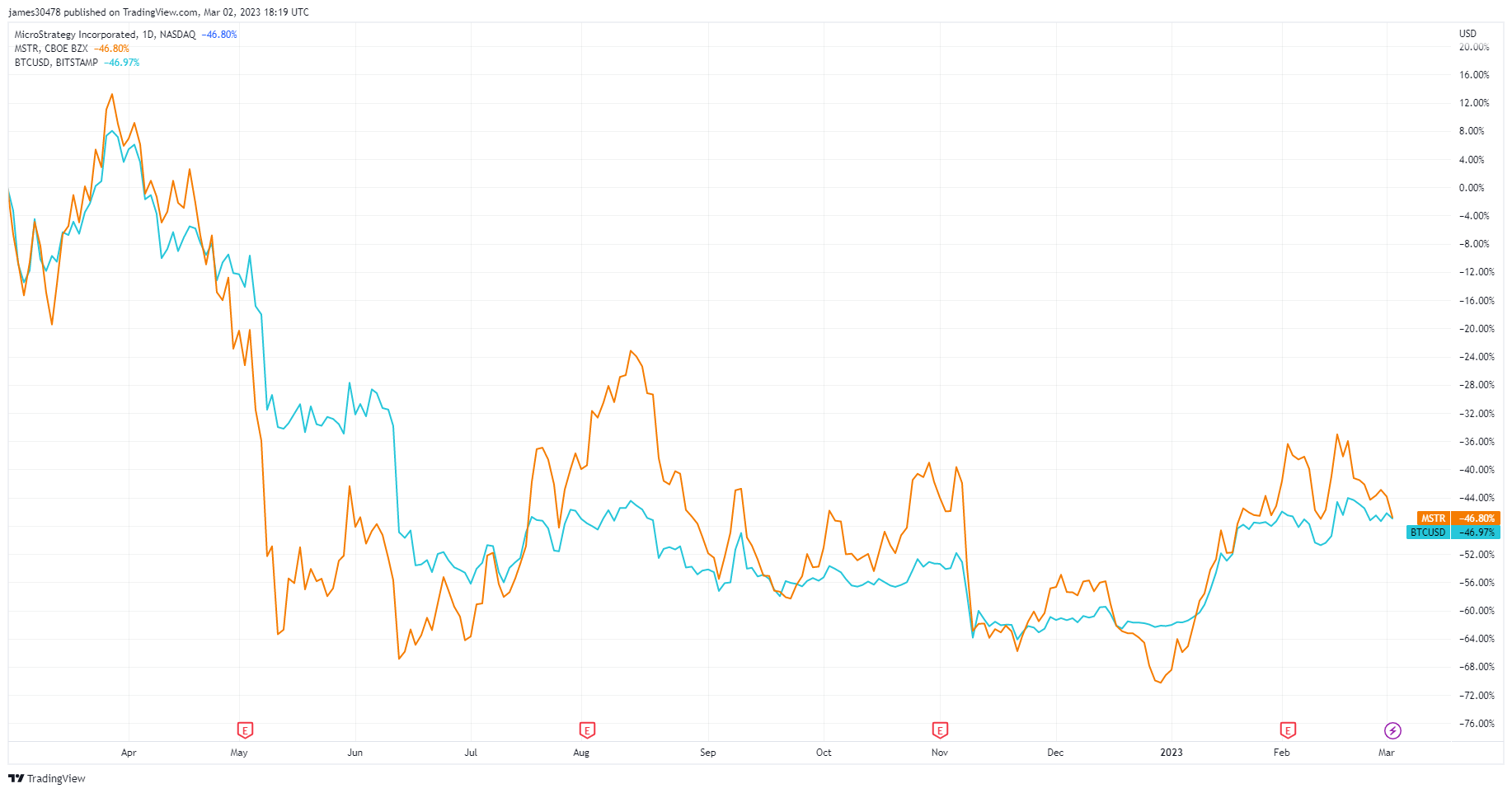

MSTR tracked Bitcoin’s performance on a one-year scale, with both seeing a 46% loss.

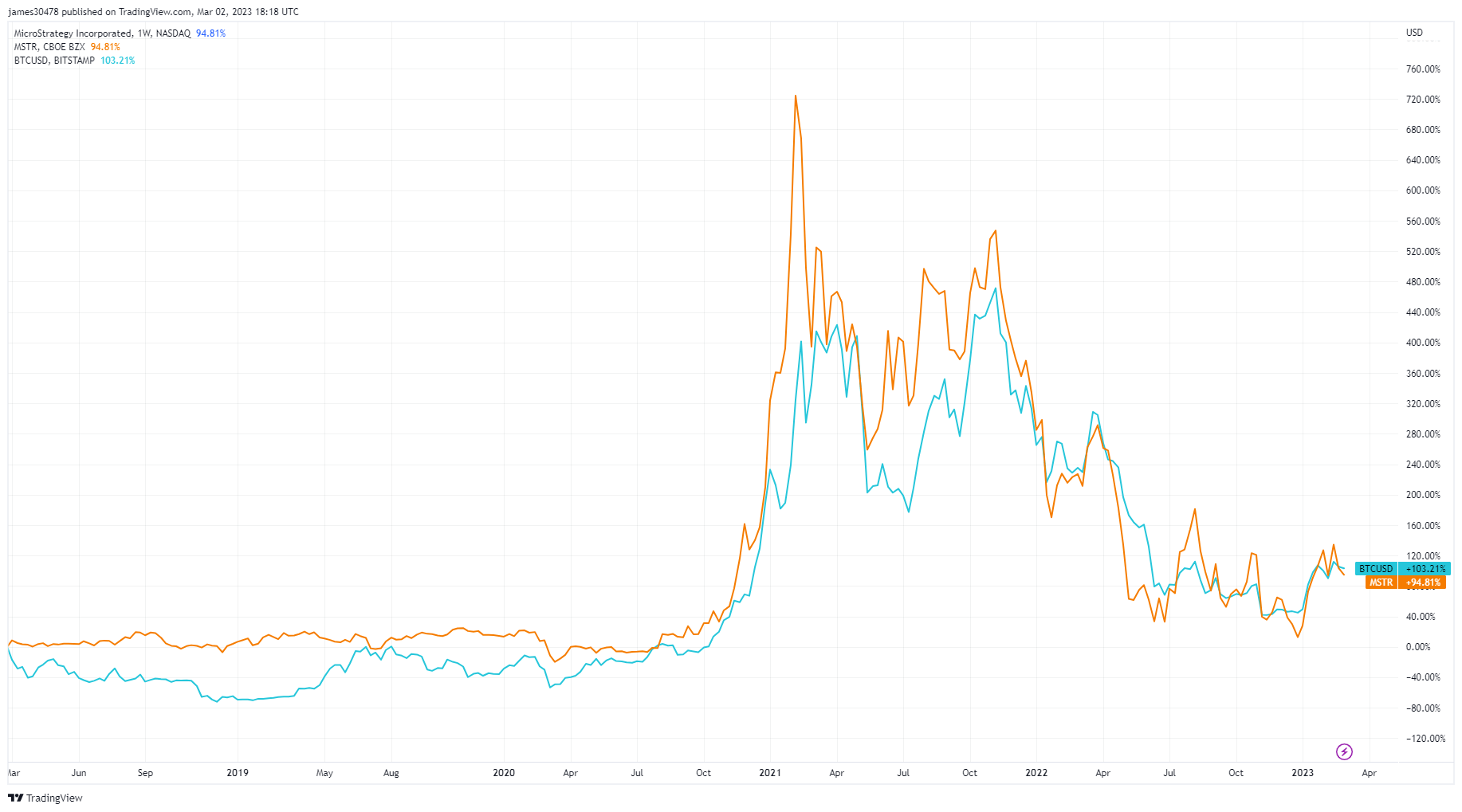

Zooming out to a five-year period shows a noticeable performance correlation, with BTC slightly outperforming MSTR with a 103% increase.

However, MSTR’s market performance has often been overshadowed by MicroStrategy’s deteriorating financial statements. At the end of the fourth quarter of 2022, the company reported an operating loss of $249.6 million, compared to $89.9 million in the fourth quarter of 2021. This brought the company’s total operating loss for 2022 to $1.46 billion.

The accounting puzzle

With an operating loss of $0.1.46 billion in 2022, a risky loan that may require new collateral, and a volatile crypto market behind it, MicroStrategy certainly doesn’t seem overvalued.

However, the company’s reported operating loss could cloud its profitability. Namely, the SEC requires companies to report quarterly unrealized losses on their Bitcoin holdings as impairments. According to MicroStrategy’s Bitcoin accounting treatment, the company’s loss in value is in addition to its operating loss. This means that a negative change in Bitcoin’s market price appears as a substantial loss on MicroStrategy’s quarterly statements, even if the company has not sold the asset.

On December 31, 2022, the company announced a $2.15 billion impairment loss on its Bitcoin holdings for the year. It reported an operating loss of $1.32 billion before tax.

Conclusion

Given MSTR’s correlation to Bitcoin’s performance, a bull market rally could take the stock back to its 2021 high.

The traditional financial market has always struggled to keep up with the pace of rapid growth seen in the crypto industry. The kind of volatility the crypto market has grown accustomed to, both positive and negative, is still rare in the stock market. In a bullish rally similar to the one that took Bitcoin to its ATH, MSTR could significantly outperform other tech stocks, including large-cap giants FAANG.

However, while MSTR’s growth may mimic the growth seen in the crypto market, the company is highly unlikely to experience significant stock price volatility over the next couple of years. If MicroStrategy continues to service its debts, it will be extremely well positioned to reap the benefits of a crypto-heavy market over the next decade.

Its long-standing reputation could make it a go-to proxy for institutions to gain exposure to Bitcoin, creating demand that keeps buying pressure high.